How do I apply for financial aid?

What is the FAFSA (Free Application of Federal Student Aid) form?

What does the cost of attendance (COA) mean?

What is the Expected Family Contribution?

What information do I need to be able to file a FAFSA?

What do I do if I’m told I’ve been selected for verification?

Will my financial aid package change each year?

What if my financial situation has changed since my prior-prior year taxes were filed?

My parents are currently separated or divorced, which should I use on the FAFSA?

What is the difference between Direct Subsidized Loans and Direct Unsubsidized Loans?

How do I apply for a Federal Direct Loan?

What is a Direct PLUS Loan for parents?

What if my parent(s) are declined the Federal Direct PLUS Loan for Parents?

How does my parent apply for the Direct PLUS Loan?

How do I apply for financial aid?

By completing the Georgetown College application and being admitted, you are eligible to receive financial aid from the College. If you are interested in any need-based aid (federal, state, and additional college aid), you will need to file a FAFSA (http://studentaid.gov/).

If you are looking for additional scholarships, please check with your high school guidance counselor, or you may look at the Georgetown College link for outside scholarships (svu7.shorinji-kempo.net/admissions/financing-your-education/scholarships). It is important to remember never pay for an outside scholarship.

What is the FAFSA (Free Application of Federal Student Aid) form?

To apply for federal student aid, such as federal grants, work-study, and loans, you need to complete the Free Application for Federal Student Aid (FAFSA) form. Completing and submitting the FAFSA form is free and easier than ever, and it gives students access to the largest source of financial aid to help pay for college.

The website is now compatible with mobile devices such as smartphones or tablets, making it even easier for the student to complete. There will be a mobile app for the FAFSA application launching in late summer 2018.

In addition, many states and colleges use your FAFSA information to determine your eligibility for state and school aid. Additionally, some private financial aid providers may use your FAFSA information to determine whether you qualify for their aid.

October 1st is the date that the FAFSA becomes available to complete. Be sure to file your FAFSA as quickly as possible beginning October 1st to ensure that you will receive as much federal funded financial aid as possible.

What does the cost of attendance (COA) mean?

Your COA is the amount it will cost you to go to school. Your COA includes tuition, room and board, and other fees before any financial aid is applied. Georgetown College will calculate your COA to show your total cost for the school year (for instance, for the fall semester plus the spring semester). Your COA is subject to change each academic year. Essentially, your COA is your budget for the year and is used to determine the financial aid you are eligible to receive.

What is the Expected Family Contribution?

Your EFC is a calculated number that college financial aid staff use to determine how much financial aid you would receive if you were to attend their school. The information you report on your FAFSA is used to calculate your EFC.

The EFC is calculated according to a formula established by law. Your families taxed and untaxed income, assets, and benefits (such as unemployment or Social Security) all could be considered in the formula. Also considered are your family size and the number of family members who will attend college or career school during your filing year.

What information do I need to be able to file a FAFSA?

The FAFSA questions ask for information about you (your name, date of birth, address, etc.) and about your financial situation. Depending on your circumstances (for instance, whether you’re a U.S. citizen or what tax form you used), you may be required to provide the following information or documents as you fill out the FAFSA:

- Your Social Security number (it’s important that you enter it correctly on the FAFSA form!)

- Your parents’ Social Security numbers if you are a dependent student

- Your driver’s license number if you have one

- Your Alien Registration number if you are not a U.S. citizen

- -Federal tax information or tax returns including IRS W-2 information, for you (and your spouse, if you are married), and for your parents, if you are a dependent student:

- IRS 1040, 1040A, 1040EZ

- Foreign tax return

- Tax return for Puerto Rico, Guam, American Samoa, the U.S. Virgin Islands, the Marshall Islands, the Federated States of Micronesia, or Palau

- Records of your untaxed income, such as child support received, interest income, and veteran’s non-education benefits, for you, and for your parents if you are a dependent student

- Information on cash; savings and checking account balances; investments, including stocks and bonds and real estate (but not including the home in which you live); and business and farm assets for you, and for your parents if you are a dependent student

What do I do if I’m told I’ve been selected for verification?

You might see a note on your Student Aid Report saying you have been selected for verification; or the Office of Student Financial Planning might contact you to inform you that you have been selected. Verification is the process Georgetown College uses to confirm that the data reported on your FAFSA form is accurate. Typically, the Department of Education determines which student the Office of Student Financial Planning is required to verify. The Office of Financial Planning has the authority to contact you for documentation that supports the information you reported.

If you’re selected for verification, don’t assume you’re being accused of doing anything wrong. Some people are selected at random. All you need to do is provide the documentation the Financial Planning Office asks for—and be sure to do so by the time the semester begins, otherwise you won’t be able to receive financial aid.

If you used the Internal Revenue Service Data Retrieval Tool (IRS DRT) when filling out your FAFSA form, you may not have to verify that information. If you didn’t use the IRS DRT, or if you filed an amended tax return and used the IRS DRT, your school may require you to submit a tax transcript as part of the verification process. You can find your tax transcript through the IRS’s Get Transcript service at irs.gov/individuals/get-transcript.

Will my financial aid package change each year?

Federal and State funded aid can change from year to year. Subsidized loan amounts and need-based aid can change based on the EFC for each year. Merit-based aid should not change unless your standing with the college changes, for example, if you fall behind on hours, GPA, living situation, etc.

You will be made aware of any changes between academic years when you receive your Financial Aid Award Letter each year.

What if my financial situation has changed since my prior-prior year taxes were filed?

The college can consider a current financial situation through a process called professional judgment. Professional Judgment refers to the authority of a school's financial aid administrator to adjust the data elements on the FAFSA and/or to override a student's dependency status. Typically, additional documentation will be required and depending on the circumstances, the Student Financial Planning Office will determine what documents are needed to complete the process. Once a professional judgment is completed, the financial aid administrator will then determine if the student qualifies for additional financial aid.

My parents are currently separated or divorced, which should I use on the FAFSA?

Whichever parent a student spends 51% of their time living with, will be the parent listed on the FAFSA.

What is the difference between Direct Subsidized Loans and Direct Unsubsidized Loans?

Direct Subsidized Loans have slightly better terms to help out students with financial need.

Direct Subsidized Loans:

- Direct Subsidized Loans are available to undergraduate students with financial need.

- Based on hours and need, the college determines the amount you are eligible to borrow.

- The U.S. Department of Education pays the interest on a Direct Subsidized Loan

- While you’re in school at least half-time,

- The first six months after you leave school (referred to as a grace period), and

- During a period of deferment (a postponement of loan payments).

Note: When a student graduates or falls below half-time, the loans will enter repayment after a 6 month grace period on the principal amount.

Direct Unsubsidized Loans:

- Direct Unsubsidized Loans are available to undergraduate and graduate students; there is no requirement to demonstrate financial need.

- The college determines the amount you can borrow based on your cost of attendance and other financial aid you receive.

- You are responsible for paying the interest on a Direct Unsubsidized Loan during all periods.

- If you choose not to pay the interest while you are in school and during grace periods and deferment or forbearance periods, your interest will accrue (accumulate) and be capitalized (that is, your interest will be added to the principal amount of your loan).

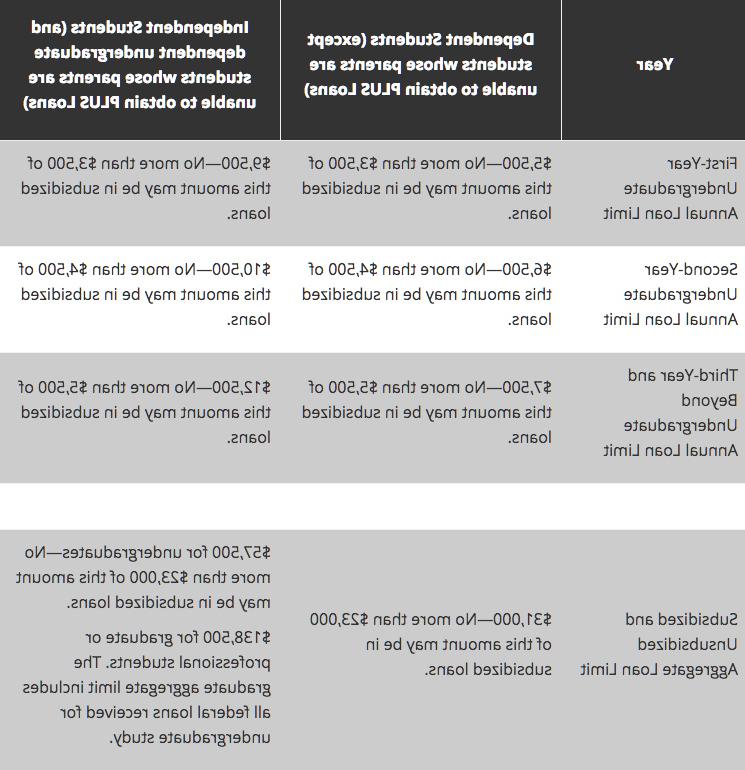

How much can I borrow?

The college determines the loan type(s), if any, and the actual loan amount you are eligible to receive each academic year. However, there are limits on the amount in subsidized and unsubsidized loans that you may be eligible to receive each academic year (annual loan limits) and the total amounts that you may borrow for undergraduate and graduate study (aggregate loan limits). The actual loan amount you are eligible to receive each academic year may be less than the annual loan limit. These limits vary depending on

- Credit hours earned

- Dependent or independent student.

If you are a dependent student whose parents are ineligible for a Direct PLUS Loan (studentaid.ed.gov/sa/types/loans/plus), you may be able to receive additional Direct Unsubsidized Loan funds.

The following chart shows the annual and aggregate limits for subsidized and unsubsidized loans.

How do I apply for a Federal Direct Loan?

You must first complete and submit the Free Application for Federal Student Aid (FAFSA®) form (studentaid.ed.gov/sa/fafsa). The college will use the information from your FAFSA form to determine how much student aid you are eligible to receive. Direct Loans are generally included as part of your financial aid package.

If your financial aid package includes federal student loans, you will need to “accept” the loan by signing and accepting your Financial Aid Award Letter.

If it is your first time receiving a Direct Loan, you will be required to

- Complete entrance counseling (studentaid.ed.gov/sa/fafsa/next-steps/entrance-counseling), a tool to ensure you understand your obligation to repay the loan.

- Sign a loan contract called a Master Promissory Note (studentaid.ed.gov/sa/fafsa/next-steps/accept-aid/mpn), agreeing to the terms of the loan.

Both the entrance counseling and the Master Promissory Note can be completed at studentloans.gov/myDirectLoan/index.action.

Federal Direct Parent PLUS Loan

What is a Direct PLUS Loan for parents?

Direct PLUS Loans are loans available to parents of dependent undergraduate students to help pay for educational expenses up to the cost of attendance minus all other financial assistance. Interest is charged during all periods.

Parents completing an electronic PLUS MPN or applying for a PLUS loan must use their own FSA ID, and not their child's FSA ID.

What if my parent(s) are declined the Federal Direct PLUS Loan for Parents?

You may either obtain an endorser (studentloans.gov/myDirectLoan/index.action), or you may choose to document to the satisfaction of the U.S. Department of Education that there are extenuating circumstances related to your adverse credit history. Once either of these courses of action has been completed, your parent will then be required to complete PLUS Credit Counseling on studentloans.gov (studentloans.gov/myDirectLoan/index.action).

Contact the Student Financial Planning Office as soon as possible to let them know whether you plan to pursue a Direct PLUS Loan by obtaining an endorser or submitting documentation of extenuating circumstances.

If you decide not to pursue a Direct PLUS Loan, the school's financial aid administrator may be able to provide information concerning other options to assist you with paying for your or the student's education.

If your parent is declined the Direct PLUS Loan, you may be eligible for additional unsubsidized loan funds.

How does my parent apply for the Direct PLUS Loan?

First-time borrowers must submit a Master Promissory Note (MPN), but every year a parent would like to utilize the Direct PLUS Loan, they must apply for the loan. You can complete both the MPN and apply for a PLUS loan at studentloans.gov/myDirectLoan/index.action.

Parents completing an electronic PLUS MPN or applying for a PLUS loan must use their own FSA ID and not their child's FSA ID. Be sure that the parent is listed as the borrower, and not the student.

Approval for the Direct PLUS Loan is credit-based, and the applicant is given an immediate decision after completing the application. The application must be completed each academic year, no matter the credit decision.

What are the options for paying for tuition?

Students may choose to pay their tuition per semester with a check or credit card to our Office of Student Accounts (502-863-8700).

Students may also choose to enroll in the monthly payment plan offered through Tuition Management Systems. We suggest that students contact the Business Office before setting up the monthly payments to get the total amount due. Students can enroll in the payment plan by going to http://mycollegepaymentplan.com/georgetown/.

Is a private student loan an option?

The college accepts private student loans as an option to cover any balance and student expenses. These loans are credit-based and can be applied for in a student or parent name. If the loan is applied for in a student’s name, the student will typically need a co-signer.

Private loans must be applied for each academic year. Private Parent loans can be in a parent’s name or any person willing to pay on the loan. The applicant can be a parent, grandparent, family friend, etc. as long as the applicant’s credit is approved.

For further information about receiving financial aid from Georgetown College, please visit our Financial Planning section.